10 MIN READ

Storage in 2024

- Self Storage Industry

6 MIN READ

March 31, 2025

|

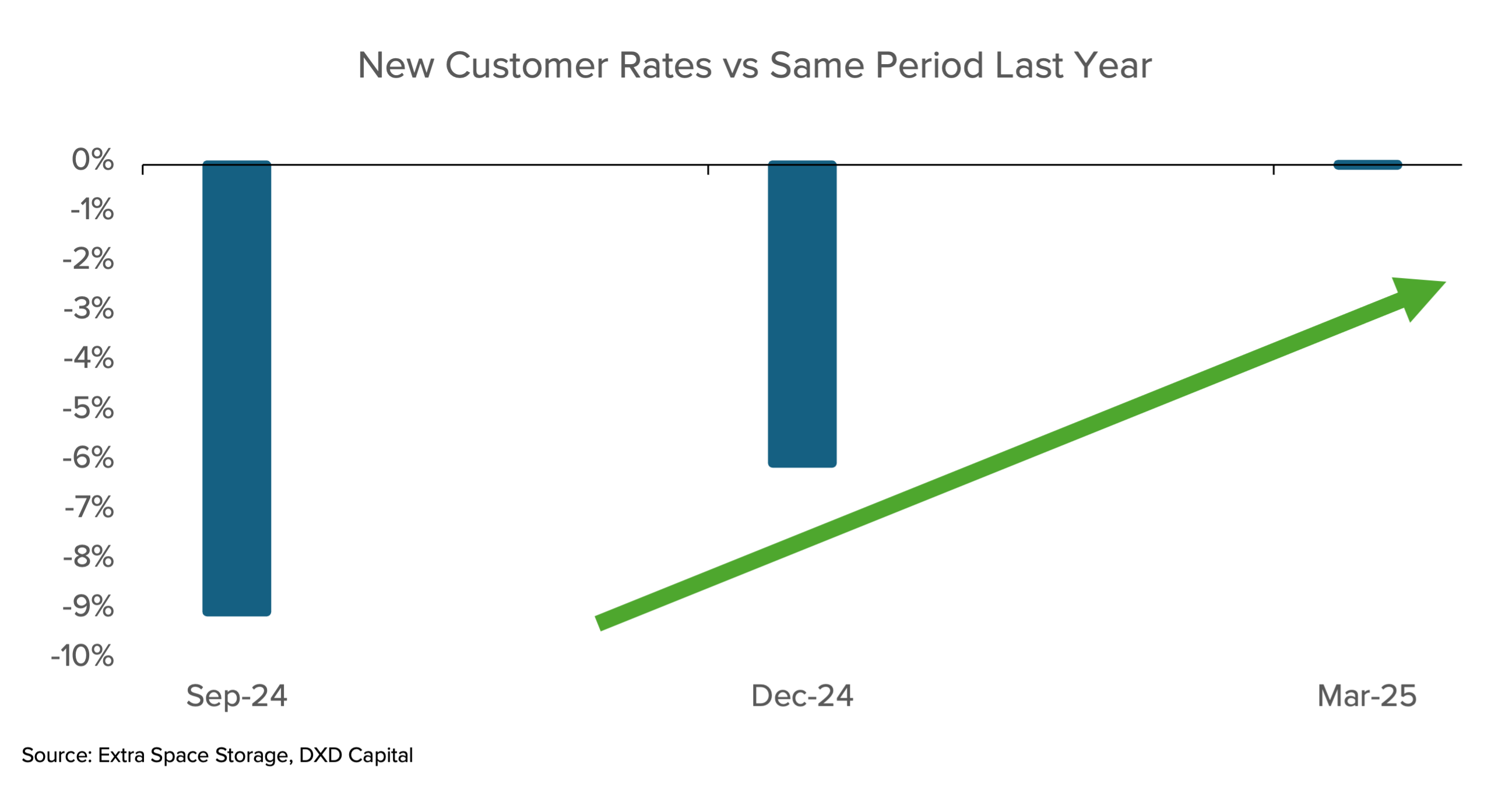

Earlier this month, Extra Space Storage and Public Storage offered valuable commentary during their annual earnings conference calls. Here are some of the important highlights: Pricing Power: We’ve Found Stable Ground Throughout 2024, the introductory (teaser) rates offered to new customers underwent a steady decline. These lower rates were due to a mix of strategy shifts in how the REITs obtained new customers combined with lower moving activity softening demand. Those declines are now behind us. Moving forward, as moving activity has also bottomed, we have now put a bottom in. In time rates will rebound but that will largely be a function of housing activity over the near term. |

|

|

|

|

|

|

Occupancy: Stability Over Surge Occupancy is stable. 48% of rentals are due to customers moving, down from 63% in 2021. This reflects a slower housing market, which is something we’ve discussed for some time. Neither company expects significant change in the demand trajectory for 2025. With interest rates being the largest impacting factor, this is DXD’s view as well. Supply Trends: A Slowing Pipeline Both companies discussed how higher costs and regulatory hurdles are curbing development—some areas remain active, but the trend favors less competition. This is consistent with what we’ve been seeing across the country. |

|

|

|

|

|

|

Slower supply is the gift that will continue giving over the next few years as we deliver our remaining Fund II assets. We have also seen a more competitive construction bid environment which has been a byproduct of fewer new storage developments. Contractors are increasingly slashing their own margins and taking a more aggressive approach to win our business, even as material cost uncertainty rises. 2025: Where to from here? We don’t expect any meaningful pickup in the housing market, as rates are likely to stay near current levels. With the Trump Administration essentially pushing austerity through the government through its DOGE efforts, I do see a potential for lower rates and higher moving activity, and it would look something like this: DOGE is reducing government spending—rather dramatically. In the event that reduction does lower inflation, coupled with higher unemployment, this could essentially pave the way for the Federal Reserve to become more aggressive in lowering interest rates. As unfavorable of a scenario as that may sound, it's my view that it would be a net benefit to storage demand as the resulting increase in moving activity would more than offset any drag from slower economic growth. With the uncertainty around Tariffs and the inflationary impact they cause, the scenario above is only one of what could transpire. The commentary from the recent FMOC meeting likely puts fewer cuts on the immediate horizon, but the environment is very dynamic and could change next quarter. Regardless of what transpires, we continue to remain bullish on self storage development and are excited to continue moving through 2025. |

LOAD MORE

2 MIN READ

4 MIN READ