7 MIN READ

3 MIN READ

June 27, 2026

FIFA is predicting $3-$4 billion in combined revenue from ticket and hospitality sales at the World Cup. That’s up 5X from the Qatar World Cup and highlights the wealth and desirability of cheering on your country in the USA. FIFA’s masterstroke was in expanding the teams from 32 to 48, increasing games from 64 to 104, and putting it in a location that has drawn and will continue to draw money to buy tickets at outrageous prices. That bet, certainly, is playing out in FIFA’s favor better in the US than it would have in other countries.

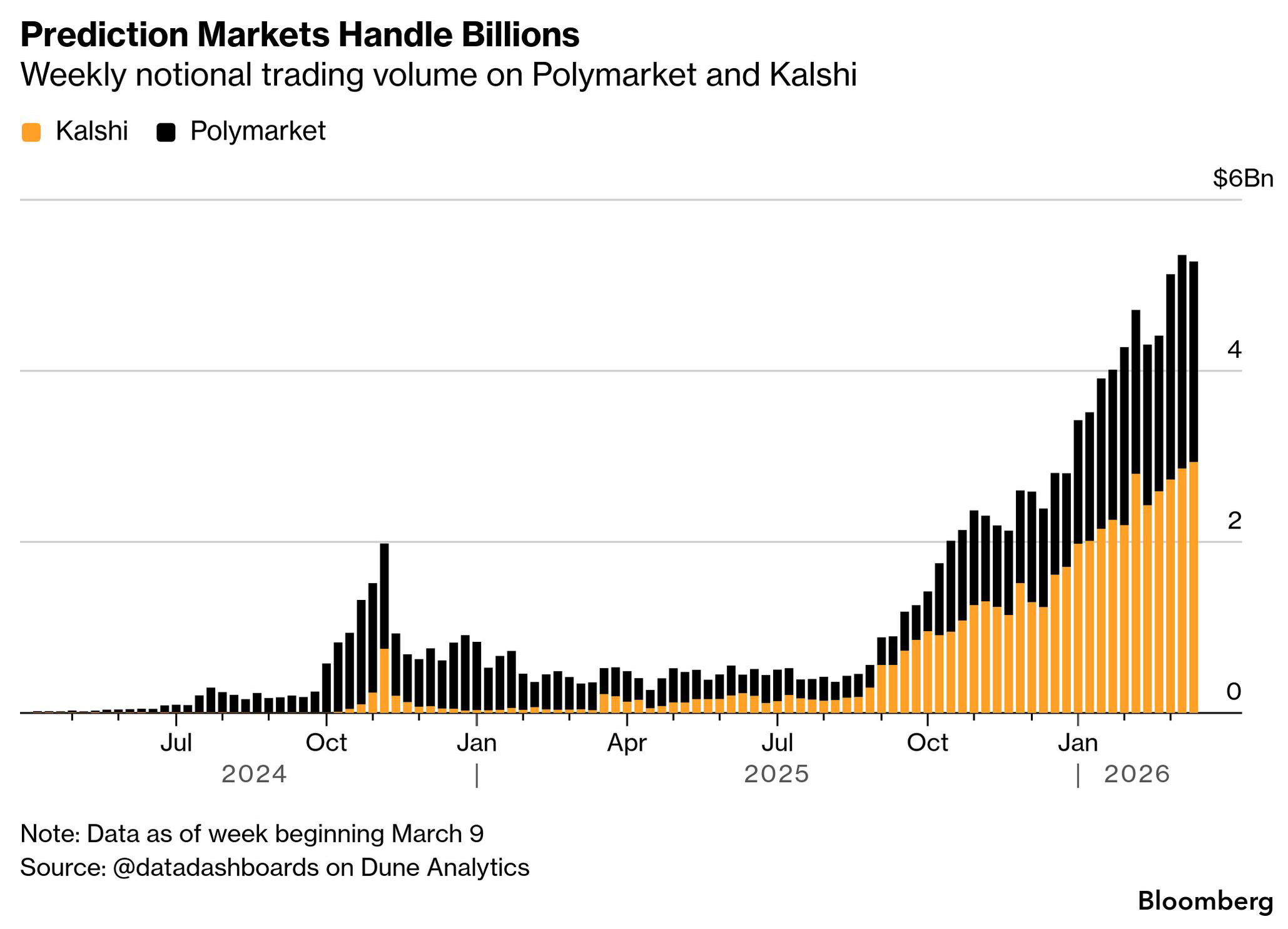

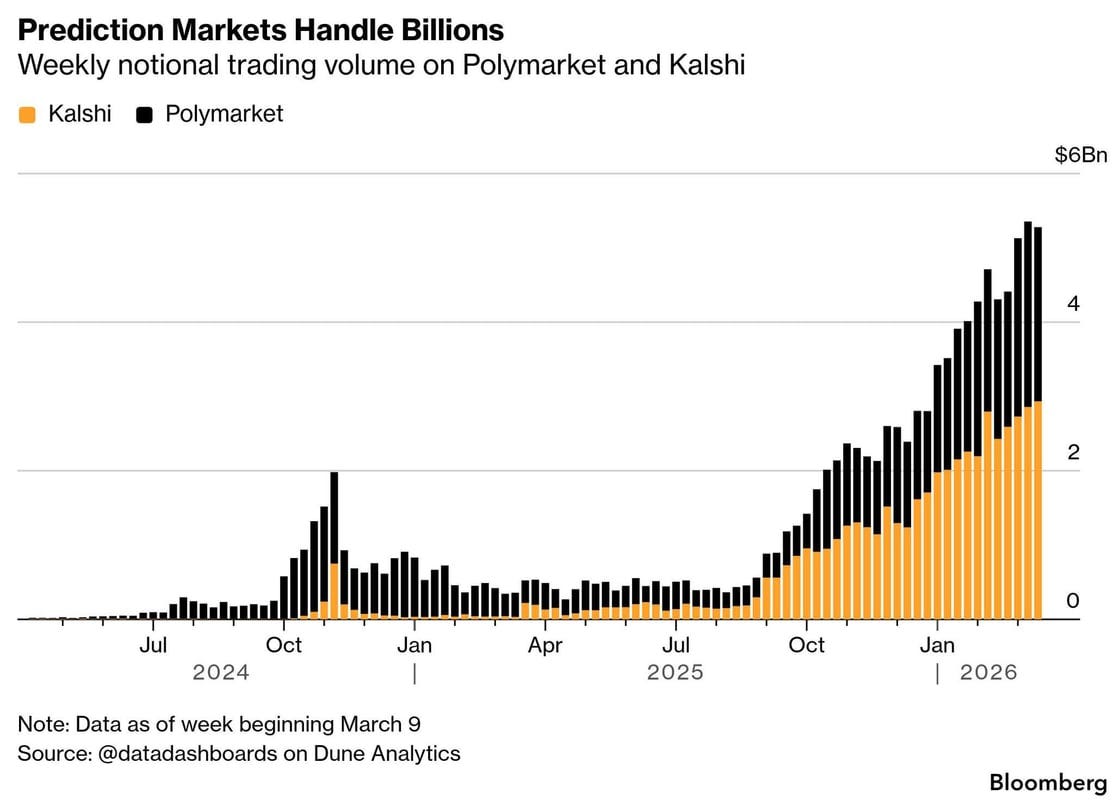

If the total World Cup revenue hits $4 billion, it’s a fraction of the estimated $60 billion in tournament betting. To put it in perspective, FanDuel and Bet365 estimate processing 100,000 bets per minute at key moments during the cup. This is all legal wagering. These betting platforms were around for the 2022 World Cup, however, the prediction platforms like Kalshi and Polymarket were not. Not only are prediction markets instantly gratifying, but they have also given a younger generation of Americans the idea that speculating is a quicker way to create wealth than homeownership.

Financial Nihilism is the belief that the economic system no longer rewards savings or long-term planning. The rise of the prediction markets has blurred the line between trading and gambling, creating a sense of wealth creation for young people rather than what it really is, pure speculation. Once, betting was a pastime, as Gen Z sees their job opportunities fade with AI, they are taking matters into their own hands and creating their own vision of financial security.

Nearly 20% of investors under 30 hold only cryptocurrency, with no stocks or real estate in their portfolios. This trend is fueled by endless social media content on platforms like YouTube, X, and Instagram that promotes quick wealth, while slower, more traditional approaches are deemed impossible.

This shift isn’t Gen Z’s fault; they are simply adapting to the challenges they face. Skyrocketing home prices, job insecurity, and shrinking purchasing power have left them seeking alternatives. To put this into perspective, in 1990, the median wage for someone with a bachelor’s degree was $58,000. Today, it’s $60,000. Imagine how discouraging it must feel to struggle just to survive, with homeownership dismissed as an unattainable dream.

How this all plays out is anyone’s guess, but it’s creating a generation of very vulnerable Americans.

See More Posts

LOAD MORE

16 MIN READ

Self-Storage Development and Zoning Activity: July 2023

- Self Storage Industry

1 MIN READ

Daytona Sees Influx of Migration from Eastern Seaboard

- Self Storage Industry