4 MIN READ

4 MIN READ

May 07, 2026

For the past four years, one narrative has dominated the housing market: homeowners are locked in. With a sub-4% mortgage on the books, why on earth would anyone sell into a 7% rate environment? That inertia has been the single biggest reason home sales have sat near historic lows and, by extension, the single biggest reason storage demand has been treading water.

That narrative is starting to crack. And Texas is showing us how.

The Data Is Moving Fast

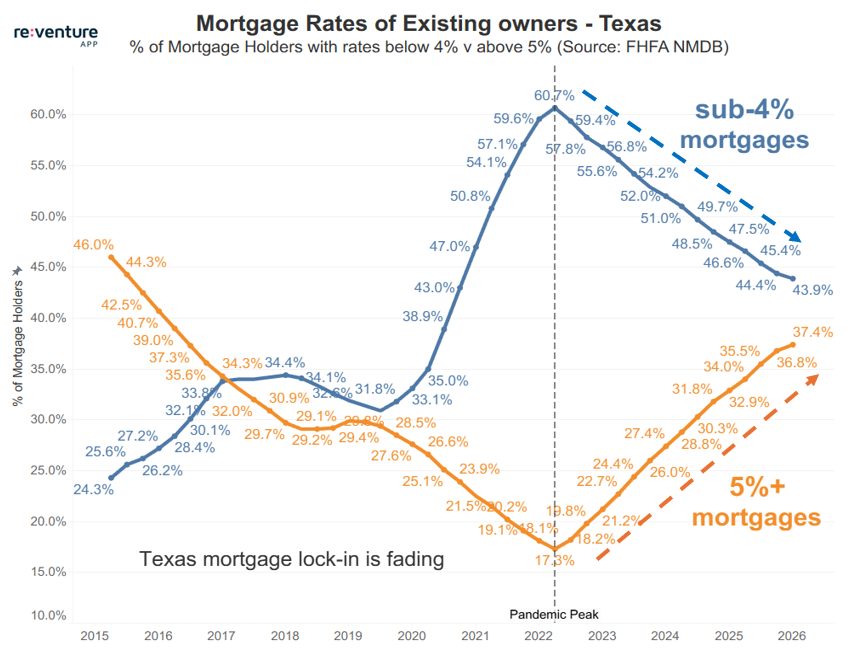

Take a look at the chart below. In 2022, at the peak of the pandemic, 60.7% of Texas mortgage holders had a rate below 4%. Only 17.3% had a rate of 5% or higher. That's a 3.5x gap and an enormous structural reason for people to stay put.

Fast forward to 2026, and those two lines are nearly on top of each other. Sub-4% mortgages have fallen to 43.9% of holders. 5%+ mortgages have climbed to 37.4%. The gap has collapsed from 43 percentage points to roughly 6.

This didn't happen because rates came down. It happened because of turnover.

Every month, older low-rate loans are paid off, refinanced, or sold. Every new purchase or refi in this environment gets written at market rates. Mortgage lock-in, it turns out, has a half-life.

Why It Matters for Storage

The lock-in effect has been the primary governor on housing transaction volume, and housing transaction volume is the primary driver of new storage demand. Roughly half of storage rentals come from people moving. When moves freeze, a large portion of storage rentals freeze with them.

What the Texas data tells us is that the governor is slowly being removed. As more owners carry market-rate payments, the calculus changes. A vacant rental property at 7.2% is far harder to sit on than one at 3.1%. An underwater homeowner who loses a job doesn't have the luxury of waiting. Price cuts, listings, and moves all follow.

Texas and Florida are leading this shift because they've seen the most new construction, the most in-migration, and the most mortgage origination activity over the past four years. Those markets turn over faster. The rest of the country is behind them, but moving in the same direction.

The Setup from Here

We've written before that meaningful recovery in storage pricing power depends on a recovery in housing activity. The REITs have been saying the same thing. What's changing is the mechanism by which housing unfreezes.

For two years, the consensus has been that housing activity returns only when mortgage rates fall. The lock-in data suggests a second path: housing activity returns when lock-in simply ages out. Owners become sellers not because rates dropped, but because the gap between their rate and the market rate shrank to the point where staying put no longer made financial sense.

Both paths end in the same place, with more moves, more storage demand, and a return to the sustained rental rate growth that has defined the sector over the last 20 years. We may get lower rates, too. But we no longer need to.

Meanwhile, new storage supply continues to slow, construction bids keep getting sharper, and the REITs are posting their first positive rate trends in years. The ingredients for the next leg of the storage cycle are quietly getting assembled.

We remain focused on building as many high-quality projects as possible while the rest of the market waits for a signal that, in states like Texas, is already here.

That narrative is starting to crack. And Texas is showing us how.

The Data Is Moving Fast

Take a look at the chart below. In 2022, at the peak of the pandemic, 60.7% of Texas mortgage holders had a rate below 4%. Only 17.3% had a rate of 5% or higher. That's a 3.5x gap and an enormous structural reason for people to stay put.

Fast forward to 2026, and those two lines are nearly on top of each other. Sub-4% mortgages have fallen to 43.9% of holders. 5%+ mortgages have climbed to 37.4%. The gap has collapsed from 43 percentage points to roughly 6.

ISource: FHFA NMDB via Reventure App

This didn't happen because rates came down. It happened because of turnover.

Every month, older low-rate loans are paid off, refinanced, or sold. Every new purchase or refi in this environment gets written at market rates. Mortgage lock-in, it turns out, has a half-life.

Why It Matters for Storage

The lock-in effect has been the primary governor on housing transaction volume, and housing transaction volume is the primary driver of new storage demand. Roughly half of storage rentals come from people moving. When moves freeze, a large portion of storage rentals freeze with them.

What the Texas data tells us is that the governor is slowly being removed. As more owners carry market-rate payments, the calculus changes. A vacant rental property at 7.2% is far harder to sit on than one at 3.1%. An underwater homeowner who loses a job doesn't have the luxury of waiting. Price cuts, listings, and moves all follow.

Texas and Florida are leading this shift because they've seen the most new construction, the most in-migration, and the most mortgage origination activity over the past four years. Those markets turn over faster. The rest of the country is behind them, but moving in the same direction.

The Setup from Here

We've written before that meaningful recovery in storage pricing power depends on a recovery in housing activity. The REITs have been saying the same thing. What's changing is the mechanism by which housing unfreezes.

For two years, the consensus has been that housing activity returns only when mortgage rates fall. The lock-in data suggests a second path: housing activity returns when lock-in simply ages out. Owners become sellers not because rates dropped, but because the gap between their rate and the market rate shrank to the point where staying put no longer made financial sense.

Both paths end in the same place, with more moves, more storage demand, and a return to the sustained rental rate growth that has defined the sector over the last 20 years. We may get lower rates, too. But we no longer need to.

Meanwhile, new storage supply continues to slow, construction bids keep getting sharper, and the REITs are posting their first positive rate trends in years. The ingredients for the next leg of the storage cycle are quietly getting assembled.

We remain focused on building as many high-quality projects as possible while the rest of the market waits for a signal that, in states like Texas, is already here.

See More Posts

LOAD MORE