3 MIN READ

Home Buying Challenges Weigh Heavily on Americans

- Real Estate Development

- Self Storage Industry

4 MIN READ

November 22, 2025

|

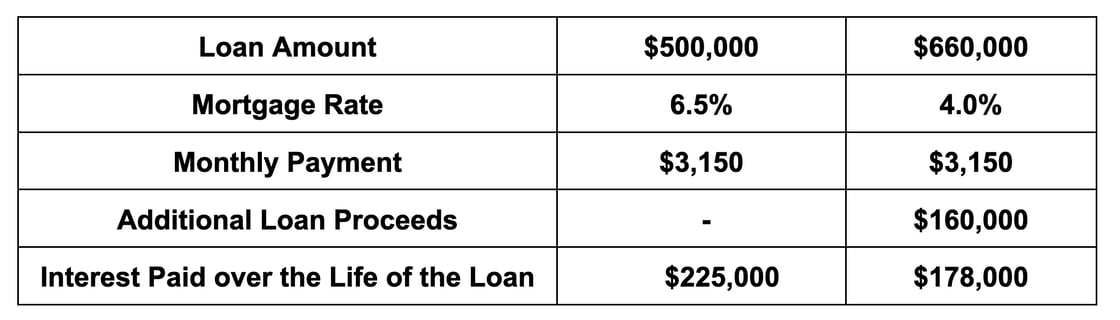

Continuing with last week's discussion on homeownership, new home builders are zeroing in on what matters most to buyers: mortgage rates. While the price of a home plays a role in purchasing decisions, the key factor is the monthly payment. If the buyer can afford the payment, the home's price becomes a secondary metric. This is the strategy builders are leveraging today—buying down the interest rate to reduce monthly payments for new buyers. However, what many buyers overlook is the impact this has on the actual price of the home. This strategy is incredibly valuable—if you're builder.

Percentage of Loans Currently Underwater

Builder financing is consistently producing more underwater homeowners. That’s not a coincidence. There’s some FOMO among first-time homebuyers that they’ve missed out on the significant 56% increase in home value appreciation over the past five years. Real appreciation over time can offset the impact of overpaying, but should we expect similar growth moving forward? My gut says absolutely not—unless interest rates return to pre-pandemic levels. The pandemic created a unique situation: historically low interest rates, a strong desire to relocate, and government stimulus. |

LOAD MORE

3 MIN READ